Dysprosium Prices

Current Dysprosium price: $930.70 per kg.

Price as of Jul 16 2026. The price shown above is the retail price for private investors and is aligned with industry retail pricing. For bulk dysprosium purchases, whether for industrial use or investment, please contact us for a quotation.

Dysprosium price performance over time

| Period | Dysprosium price then | Change to today |

|---|---|---|

| Current price | $930.70/kg | — |

| 1 year | $453.90/kg | +105.05% |

| 2 years | $386.90/kg | +140.55% |

| 3 years | $521.40/kg | +78.50% |

| 5 years | $613.70/kg | +51.65% |

| 10 years | $269.89/kg | +244.84% |

Dysprosium Historical Price Movement

Dysprosium prices have become increasingly influenced by the supply risks surrounding heavy rare earths and the growing importance of heat-resistant magnet materials.

At today’s price of $930.70 per kg,

dysprosium is

up 105.05% year to date,

up 163.58% since the start of 2025,

up 58.44% since the start of 2024,

and up 169.58% since the start of 2020,

when the dysprosium price stood at $345.24 per kg.

This reflects dysprosium’s importance in permanent magnets, nuclear shielding, glass production, and halogen lamps, combined with a market where limited extraction and concentrated rare-earth supply chains can tighten availability quickly.

Dysprosium annual price performance

| Current Dysprosium Price/kg |

2026 YTD | 2025 | 2024 | 2023 | 2022 | 2021 | 2020 |

|---|---|---|---|---|---|---|---|

| $930.70 | 105.05% | 28.55% | -39.89% | -10.10% | -15.10% | 87.21% | 19.08% |

To get a full picture of the potential price trajectory for dysprosium, let’s explore its myriad uses and delve into which countries produce it the most. Armed with this knowledge, we can make more informed predictions about what lies ahead (jump to forecast).

Dysprosium is a chemical element with the symbol Dy and atomic number 66. It is a rare earth element with a metallic silver luster.

Dysprosium is seldom encountered as a free element in nature and is usually found in minerals such as xenotime, dysprosium-yttrium fluorite, gadolinite and euxenite. 32Dy makes up about 0.06% of the Earth’s crust.

Dysprosium Uses

Dysprosium Powder

Dysprosium is one of the most critical heavy rare earths used in modern industry. Its exceptional magnetic and thermal properties make it indispensable in high-performance technologies, especially those driving the clean-energy transition.

Permanent Magnets and Green Technologies

The majority of dysprosium produced today is used in neodymium-iron-boron (NdFeB) permanent magnets, where it significantly improves resistance to demagnetization at high temperatures. These high-strength magnets power electric vehicle motors, wind turbine generators, and advanced robotics, forming the backbone of the green-tech revolution.

Nuclear, Defense, and Aerospace

Because of its neutron-absorbing abilities, dysprosium is used as an alloying element in control rods for nuclear reactors. Its stability under extreme conditions also makes it valuable in defense, aerospace, and precision guidance systems, where reliability and heat tolerance are paramount.

Specialty and Emerging Applications

Dysprosium compounds are used in lighting, laser materials, and specialty glass production. Research is expanding its use in medical imaging and diagnostic lasers, while new energy-efficient technologies continue to open additional commercial pathways.

Strategic Importance

As one of the key “energy transition metals,” dysprosium is now considered essential to the global move toward decarbonisation. The European Union, the United States, and Japan all list it as a critical raw material, citing its irreplaceable role in clean-energy manufacturing and its highly concentrated supply chain in China.

Demand for dysprosium is expected to grow steadily for decades, with analysts projecting that consumption for magnet applications alone will not peak before the 2040s, underscoring its long-term strategic importance.

Where is Dysprosium Produced?

Dysprosium occurs mainly in ion-adsorption clays, which are especially rich in the heavy rare earth elements. The highest-grade deposits are found in southern China, particularly in Jiangxi Province, where clays can contain significantly higher concentrations of dysprosium than monazite or bastnäsite ores found elsewhere.

Today, China controls over 90% of global dysprosium production, not only through mining but, more importantly, through its near-monopoly on refining and separation capacity, which remains the real bottleneck for heavy rare earths.

A large share of the raw ore processed in China originates from Myanmar, whose intermittent mine closures and border disruptions frequently tighten supply and contribute to price volatility.

Outside of China, production remains limited. Smaller volumes come from Australia, Malaysia, and Russia, while Western governments are now investing heavily in projects aimed at diversifying supply. Notably, Lynas Rare Earths has become the first commercial producer of heavy rare earths outside China, though global capacity remains far from meeting projected long-term demand.

What Factors Determine the Price of Dysprosium?

Dysprosium prices are driven by a combination of industrial demand, supply concentration, geopolitical risk, and technological trends.

1. Demand from Permanent Magnets and Green Technologies

The single biggest driver of dysprosium demand is its use in high-performance NdFeB permanent magnets, which power:

electric vehicle motors

wind turbine generators

robotics and automation

industrial motors

As nations accelerate toward low-carbon economies, magnet demand continues to rise. Analysts expect consumption for energy-transition metals like dysprosium to grow steadily into the 2040s, with no peak in sight.

2. Highly Concentrated Supply

While rare earths are relatively abundant in the earth’s crust, economically viable deposits of heavy rare earths like dysprosium are scarce. Extraction is costly, refining is complex, and over 90% of global separation capacity sits in China.

This concentration means dysprosium prices are influenced not just by mining output but by:

Chinese export restrictions

refining bottlenecks

production quotas

environmental enforcement campaigns

disruptions at Myanmar’s ion-adsorption clay mines

3. Geopolitical and Trade Dynamics

Events such as export controls, trade disputes, or border closures can have immediate price impacts, particularly because Western manufacturers have limited alternatives to Chinese supply. Recent policy shifts have shown that heavy rare earth markets are increasingly treated as strategic assets rather than simple industrial commodities.

4. Slow Supply Growth vs. Rapid Technology Adoption

Developing new rare earth mines and separation facilities takes years, often more than a decade. Meanwhile, technological adoption (EVs, wind) grows far more quickly. This mismatch frequently pushes the market into structural deficits, tightening supply and supporting higher prices.

5. Slow and Fragmented Price Reporting

The global rare earth market remains relatively opaque, with spot indices often reflecting only a small share of actual industrial trading activity. Published prices tend to lag behind real-world buyback markets, where manufacturers and refiners may adjust offers much more quickly in response to immediate needs or supply shocks.

To help private investors navigate this, we publish current dysprosium prices directly on our website, offering clear, up-to-date guidance in a market where reliable pricing is not always readily available.

Even in periods when new sales are paused, movements in the industrial buyback market can diverge significantly from published spot prices. This is why, for example, our December 2025 buyback price of $780/kg for existing clients is substantially higher than many published indices: it reflects true industrial demand in real time, rather than delayed spot-market reporting.

Summary

Dysprosium prices are shaped by a unique combination of rising long-term demand, highly concentrated supply, geopolitical leverage, and slow supply-chain development. This environment creates both opportunities and volatility, especially during periods of supply constraint.

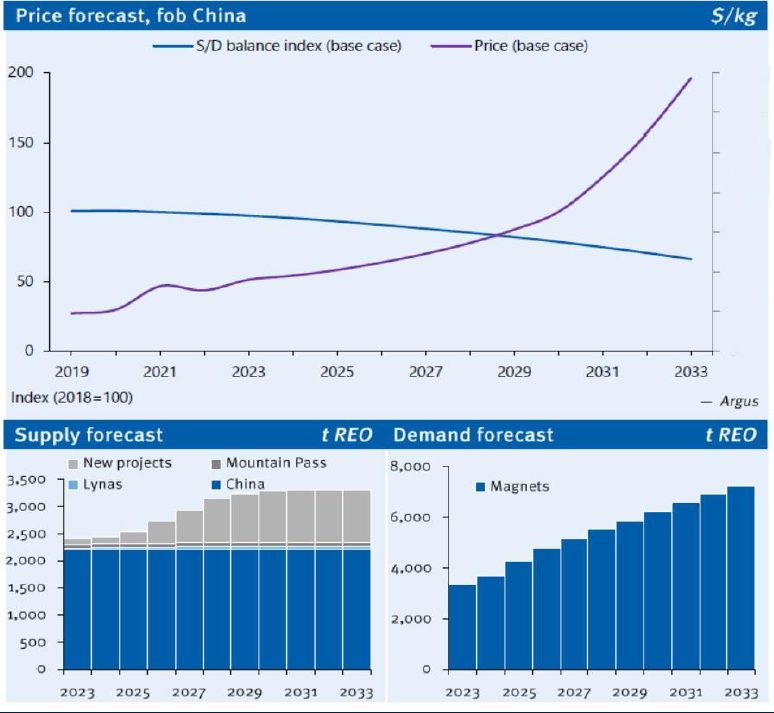

Dysprosium Price Forecast

At a glance

- Price pulse: Dysprosium rose 28.55% in 2025 on the published retail benchmark, then surged a further 105.05% in Q1 2026.

- Market character: This remains a small, strategic, politically influenced market where published prices can lag tighter industrial buy-back conditions. Our own December 2025 buy-back price of $780/kg already signalled that real industrial demand was running ahead of many published spot references.

- Supply structure: Dysprosium remains one of the most supply-constrained heavy rare earths, with China still controlling the key refining and separation bottleneck and Myanmar remaining a fragile upstream feedstock source.

- New twist: Western diversification is clearly accelerating (via Lynas, the France/Japan Caremag project, and new U.S. heavy rare earth agreements) but none of that changes near-term scarcity.

What changed for Dysprosium in 2025 and Q1 2026

Dysprosium did not just rise. It re-rated.

On the published retail benchmark, dysprosium finished 2025 up 28.55%, then exploded another 105.05% in Q1 2026 to $930.70/kg. That kind of move is not typical commodity drift. It is what happens when a tiny, strategic market suddenly starts repricing supply risk more honestly.

The underlying story is not hard to identify. China’s rare earth export-control regime remains a live constraint, and in early 2026 Beijing was still tightening oversight enough that a Chinese metals body scheduled a dedicated policy briefing for exporters. In other words, the system is not normalising. It is being managed.

At the same time, the trade data is sending a familiar message: availability may look better in aggregate than it feels in practice. Reuters reported that China’s rare-earth magnet exports rose 8.2% year on year in the first two months of 2026, yet shipments to the U.S. fell 22.5%. That is not broad relief. That is selective access.

Meanwhile, the West is moving faster, but still from far behind. Malaysia renewed Lynas’ licence for another 10 years, while the company continues investing in heavy rare earth separation capacity. Japan and France have also agreed to support the Caremag refining project, with Japan aiming to source about 20% of its future dysprosium and terbium demand from it. In the U.S., REalloys and U.S. Critical Materials signed a new MoU around a domestic heavy rare earth supply chain. All of that matters. None of it solves 2026.

What this means for Dysprosium

Dysprosium now looks less like an obscure rare earth and more like a strategic bottleneck metal.

Its price is no longer being driven only by optimism around EVs or wind turbines. It is being driven by a harsher reality: the market needs a heavy rare earth that is difficult to substitute, difficult to separate, politically sensitive, and still overwhelmingly controlled by China and its surrounding supply ecosystem.

The sharp move in Q1 2026 suggests that published benchmarks were, to some extent, catching up with industrial reality. That fits the pattern already visible in the dysprosium market: spot reporting is often slow, and industrial buy-back pricing tends to move first when material gets tight.

Price drivers tilting upward

- High-temperature magnet demand: Dysprosium remains essential in magnet chemistries where thermal stability matters, especially for electric vehicle motors, offshore wind, and defence-related applications.

- China policy premium: Export controls may pause, soften, or be discussed diplomatically, but licensing, classification and end-use controls remain a real source of friction.

- Fragile heavy rare earth chain: Myanmar-related disruption and China’s control over refining keep the market structurally exposed to sudden shortages.

- Ex-China rebuilding confirms scarcity: Every new Western or allied project reinforces the same point: dysprosium is important enough that governments are now actively trying to rebuild supply chains around it.

Potential headwinds to watch

- Short-term diplomatic easing: If tensions between China and major buyers ease, some shipments can resume faster than sentiment expects, which can cool panic pricing in the short run.

- Vertical-move fatigue: After a Q1 surge of this size, consolidation or a pause would be normal even if the broader structure stays bullish.

- Longer-dated diversification: New refining and processing projects outside China will not solve the near term, but over time they can reduce the most extreme upside scenarios.

Dysprosium 6–12 month forecast view

Bias: Bullish with high volatility

Rationale:

The fundamental setup remains tight. China still controls the choke point that matters most, and heavy rare earth markets remain highly sensitive to licensing friction, geopolitical signalling, and feedstock disruption. Even if prices cool after the vertical Q1 move, the market does not yet look loose enough for a meaningful reset lower. The more likely pattern is wide swings around a higher base.

12–24 month forecast view

Bias: Bullish

Rationale:

By this stage, some diversification efforts should start to become more visible, especially through projects like Caremag and Lynas’ expanded heavy rare earth work. But visibility is not the same as abundance. The market is still likely to treat dysprosium as a strategic material first and a normal industrial input second. That should keep a geopolitical premium embedded in prices, particularly if U.S.–China or Japan–China tensions flare again.

3–5 year forecast view

Bias: Strongly Bullish

Rationale:

Over the longer term, dysprosium still sits in a very favourable corner of the strategic metals universe: it is small, irreplaceable in key high-temperature magnet uses, difficult to scale, and now firmly recognised by governments as a supply-chain vulnerability. Even successful diversification outside China is unlikely to recreate Chinese cost structures quickly. In practice, that means more security-of-supply investment, more strategic stockpiling, and a structurally firmer long-run price floor than the market used to assume.

Why physical Dysprosium fits the Strategic Metals Invest playbook

Dysprosium fits the Strategic Metals Invest playbook because it combines four characteristics that matter most in this asset class: small market size, strategic necessity, highly concentrated supply, and the potential for industrial pricing to move faster than published spot references. Dysprosium’s recent price history already shows this in practice. By the time a market like this looks obvious on a chart, the real squeeze is often already underway.

How to Buy Dysprosium

Industry-grade dysprosium powder is usually sold at minimum 99.5% purity, priced in USD, and the weight unit is per kilogram. Safe storage is essential because, like many powders, dysprosium may constitute an explosion hazard when mixed with air and an ignition source is present.

Corporate buyers such as Tesla, BMW, Ford, and Mercedes use well-established metal dealers to buy industry-grade dysprosium. Renowned metals dealers, such as ourselves, act as key intermediaries between the high-tech industries and the producers of the critical rare earth elements needed by these industries.

Unless you purchase from a reputable dealer (e.g. if you buy on Amazon, Alibaba, or eBay), there’s no guarantee of purity and no possibility of liquidation to anyone other than hobbyists.

Any discerning investors who want to benefit from future price increases by purchasing and owning some dysprosium can do this through us. By doing so, you are buying from the only globally licensed industry supplier offering this option to private investors.

Dysprosium futures contracts can also be traded in the Shanghai Metal Market (SMM).

How to Sell Dysprosium

Please note that the only end buyers for your industrial-grade dysprosium are industry buyers such as General Motors, Honda, Tesla, Apple, and First Solar. These buyers will only buy from established industry suppliers with documentary evidence of the complete chain of custody. They don’t buy from the likes of eBay, Alibaba, or Amazon.

No industry buyer will transact with a seller that cannot provide the entire chain of custody documentation, analysis & purity reports, and proper storage facilities. We guarantee the fast and safe liquidation of the rare earth elements of our investors because we’re such an industry supplier.

All prices on this page last updated Jul 16 2026.