Praseodymium Prices

Current Praseodymium price: $245.40 per kg.

Price as of Jul 10 2026. The price shown above is the retail price for private investors and is aligned with industry retail pricing. For bulk praseodymium purchases, whether for industrial use or investment, please contact us for a quotation.

Praseodymium price performance over time

| Period | Praseodymium price then | Change to today |

|---|---|---|

| Current price | $245.40/kg | — |

| 1 year | $99.60/kg | +146.39% |

| 2 years | $95.80/kg | +156.16% |

| 3 years | $135.70/kg | +80.84% |

| 5 years | $114.00/kg | +115.26% |

| 10 years | $56.14/kg | +337.12% |

Praseodymium Historical Price Movement

Praseodymium prices are increasingly influenced by the expanding role of rare-earth magnet materials in electrification, advanced manufacturing, and clean-energy technologies.

At today’s price of $245.40 per kg,

praseodymium is

up 70.30% year to date,

up 155.36% since the start of 2025,

up 117.55% since the start of 2024,

and up 237.23% since the start of 2020,

when the praseodymium price stood at $72.77 per kg.

This reflects praseodymium’s role in permanent magnets, aircraft engines, specialised glass, and other high-performance applications, combined with a market where supply remains concentrated and vulnerable to refining bottlenecks.

Praseodymium annual price performance

| Current Praseodymium Price/kg |

2026 YTD | 2025 | 2024 | 2023 | 2022 | 2021 | 2020 |

|---|---|---|---|---|---|---|---|

| $245.40 | 70.30% | 49.95% | -14.80% | -43.15% | -8.70% | 160.55% | 14.61% |

Praseodymium is a chemical element belonging to the rare earth group of metals. It has the atomic number 59 and is represented by the symbol Pr on the periodic table. Discovered in 1885 by Carl Auer von Welsbach, praseodymium has a silvery-white color when in its purest form.

To predict where praseodymium prices may head in the future (jump to forecast), it’s important to understand its many applications and who produces it. Let’s dive deeper into this valuable metal and what role it plays globally.

Praseodymium Uses

Praseodymium’s unique properties make it indispensable across various modern industries. For decades, it has been used as an alloying agent with softer metals such as aluminum and magnesium to strengthen them without reducing flexibility, particularly in aircraft engines and turbine components.

Its most important role today is in the production of neodymium–praseodymium (NdPr) permanent magnets, which are essential for electric vehicle motors, wind turbines, and precision electronics. These magnets are prized for their combination of strength, heat resistance, and low weight, all characteristics that have made them critical to the green energy transition.

Beyond magnets, praseodymium serves as a neutron absorber in nuclear reactors and plays a role in glass manufacturing, high-intensity lighting, and lasers. Certain praseodymium compounds emit vivid red and green light, making them valuable in TV and smartphone displays.

Praseodymium also continues to attract research interest in advanced fuel cells and medical applications, where its magnetic and radiological properties are being studied for targeted therapies such as Praseodymium-177, a beta-emitting isotope used in cancer treatment.

In short, praseodymium’s versatility, from clean energy and aerospace to medical and optical technologies, highlights why it remains one of the most strategically important rare earth elements for the decades ahead.

Where is Praseodymium Produced?

Praseodymium is not mined on its own. It occurs alongside other light rare earth elements, particularly neodymium, within bastnäsite and monazite ores. Globally, China remains the dominant producer, accounting for roughly 69% of rare earth ore output in 2024 and an even larger share once separation and refining are included. Outside China, the United States, Myanmar, and Australia contribute to global supply, although each operates at a far smaller scale.

China’s dominance extends well beyond mining. It controls more than 80% of the global rare earth processing capacity, making it a critical bottleneck in the entire supply chain. Even when other countries increase extraction, much of that material is still shipped to China for refining. As a result, the real supply concentration risk lies not only in mining but in the separation and processing stages, where China’s lead remains unmatched.

While China will remain the dominant force in the near term, several countries are beginning to develop alternative sources of praseodymium supply.

Emerging Producers

Outside China, a number of countries are working to expand or establish rare earth production, although most projects remain in early stages. Australia continues to scale output through companies like Lynas, while the United States and Canada are investing in domestic mining, separation, and magnet production to reduce their reliance on Chinese processing. Exploration and development efforts in Brazil, Vietnam, and Greenland have also accelerated, reflecting broader geopolitical interest in diversifying supply chains. These initiatives are promising, but they will take years to mature, meaning China is expected to remain the central supplier of separated praseodymium well into the next decade.

What Factors Determine the Price of Praseodymium?

Praseodymium prices are driven primarily by the balance between supply and demand. As a key component of high-performance NdPr permanent magnets, demand rises with the growth of electric vehicles, wind turbines, robotics, and advanced electronics. When these sectors accelerate, the pull on praseodymium intensifies, often pushing prices higher.

On the supply side, China remains the dominant force. It controls most of the global mining and more than 80 percent of the world’s processing capacity. Changes in China’s mining quotas, export controls, or environmental policies can quickly influence availability and cause sharp price movements. In recent years, reduced transparency around quota issuance and stricter reporting requirements have added to the uncertainty in the market.

Geopolitical developments also play a significant role. Decisions by Western producers to divert material away from China, disruptions in Myanmar’s ionic clay operations, or new critical-minerals policies in the U.S. and EU can all affect the flow of rare earth feedstock and ultimately influence global praseodymium pricing.

Understanding these supply-and-demand dynamics, especially China’s policy decisions and the pace of clean-energy technologies, is key to anticipating where praseodymium prices may move in the years ahead.

Praseodymium Price Forecast

At a glance

After a 3-digit price hike in 2021 (+161%), praseodymium saw a 55% decrease in value from 2022 to 2024. However, praseodymium rebounded strongly last year, with prices gaining nearly 50%. The rally is not just “EV hype.” It rests on tighter Chinese quota management, fresh policy controls that add friction to supply, and a rare burst of Western supply chain realignment that diverted material away from China’s processors in Q3. The setup for the next 3–5 years is a classic magnets-meets-policy squeeze: demand growth that is steady, not speculative, and supply discipline that is real, not rhetorical.

What changed in 2025

1) China tightened the rulebook and blurred the scoreboard.

Beijing rolled out new interim regulations that extend quota compliance and licensing to both domestic and imported rare earth feedstock, with tougher reporting and penalties. At the same time, the first 2025 mining and smelting quotas were issued quietly, without the usual public disclosure. That opacity raises risk premia because market participants cannot easily model near-term availability. (Source: AP News)

2) A U.S. supply detour jolted prices.

In late August, MP Materials stopped shipping raw material to China as it pivots to domestic refining under U.S. government agreements. Analysts estimated this removed roughly high-single-digit percent of China’s oxide feed, and Chinese NdPr oxide prices jumped 40% in a matter of weeks, the highest in more than two years. That price action spilled over into praseodymium quotations globally. (Source: Reuters)

3) Non-China supply is inching up, but not enough.

Australia’s Office of the Chief Economist expects Australian NdPr oxide output to rise to roughly 5,750 t in 2025, up about 78% year on year. Helpful, but still small compared to Chinese separation capacity and rising global magnet demand.

4) Demand growth looks persistent, not peaky.

IEA’s 2025 critical minerals outlook still sees rare earth demand growing strongly to 2040, with permanent magnets in EV motors and wind remaining the main driver. Even with efficiency gains and thriftier magnet recipes, total magnet tonnage continues to rise with EV and wind installations.

5) Myanmar remains unreliable.

Border ionic-clay operations feed Chinese separation plants and influence heavy REEs most, but instability and environmental clampdowns keep the regional supply picture fragile across the complex. Markets price some of that risk into light REEs like NdPr when Chinese processors feel any feedstock pinch.

What this means for praseodymium

Price drivers tilting upward

Policy friction: Stricter Chinese controls on mining, smelting, imports, and reporting increase the chance of administrative bottlenecks. When quotas are opaque, buyers build precautionary inventory. That supports prices.

Western re-routing: The U.S. push to refine and magnetize at home temporarily reduces feed available to Chinese separators. That shrinks the most liquid market just as seasonal demand returns.

Steady end-use growth: EV powertrains and wind turbines remain structural sinks for NdPr magnets through 2030 and beyond, even as demand for recycling advances.

Potential headwinds to watch

Technological substitution risk: Rare-earth-free magnets are back in the headlines. A U.S. start-up claims iron-nitride magnets can compete with NdFeB on performance. If they scale, that would be material; however, the industry remains extremely cautious (we have heard similar claims before without ever any success). This is a risk to monitor rather than a near-term base case.

Supply catch-up: Australian and U.S. projects are adding units. If a synchronized ramp arrives into a softer macro patch, it could cap the upside for a few quarters.

6–12 month forecast view

Bias: Moderately bullish.

Rationale: Tighter Chinese governance, quota opacity, and U.S. feedstock re-routing have already reset price expectations. If manufacturing activity in China and seasonal magnet orders hold, praseodymium should remain well supported into 2026. The price spike triggered by MP’s shift showed how thin the spot market can be when one major flow changes course.

12–24 month forecast view

Bias: Bullish with volatility.

Rationale: Demand growth from EVs and wind is durable, while non-China supply growth looks incremental rather than explosive. Policy risk stays elevated in China. Substitution efforts are real but not yet scaled. Expect higher highs and sharper pullbacks rather than a straight line.

3–5 year forecast view

- Bias: Bullish, with episodic volatility but a rising floor.

- Rationale: By 2028–2030, the demand side should feel heavier than today, while the supply side still looks disciplined. Magnet rare earth demand growth is not a one-season story. The IEA’s 2025 outlook shows magnet REE demand climbing steadily through 2040, with EVs and wind doing most of the heavy lifting. That is the core pull on NdPr, which is where praseodymium lives.

Why physical Praseodymium fits the Strategic Metals Invest playbook for savvy investors

Praseodymium is a tangible, industry-grade material that can be resold directly to industry at any time, not a financial proxy asset.

Supply concentration risk is being managed with policy tools (from China) rather than new mines, which tends to keep the market tight and supports controlled prices over the long term.

Magnet demand will continue to grow as EV adoption expands, even if each vehicle uses slightly less magnet material.

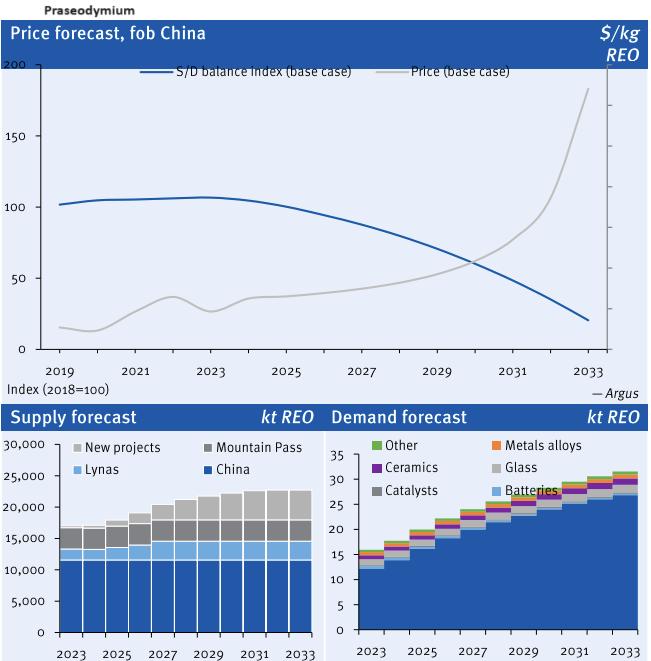

Below are 10-year forecast graphs by Argus Media for Praseodymium’s future price (fob China), demand, and supply.

How to Buy Praseodymium

Hobbyists interested in purchasing praseodymium may easily find it on sites like Amazon, Alibaba, and eBay. However, these sources offer no assurance of purity or liquidity for the buyer other than what another hobbyist is willing to pay.

For higher quality standards and greater certainty when buying this valuable rare earth metal, corporate buyers such as Samsung, Ford, Tesla, and Panasonic purchase through reputable metals dealers who serve as a bridge between high-tech industries seeking raw materials and the producers supplying them. Those that want to benefit from potential future price increases by owning some praseodymium can do so with us, knowing that they’re buying from the only licensed global industry supplier offering investors private access to this exciting asset class.

Praseodymium futures contracts are also traded in the Shanghai Metal Market (SMM).

How to Sell Praseodymium

Rare earths like praseodymium are highly sought-after by industry buyers like General Motors, LG, and Apple. However, they only purchase from reputable suppliers who can provide a full chain of custody, including analysis reports on purity levels plus adequate storage facilities.

Hence, to ensure the fast and safe liquidation of this resource for investors, it’s crucial that they source it from a reputable supplier, like ourselves, in the first place (all our praseodymium is certified min. 99% pure). Otherwise, they can only sell their praseodymium to hobbyists on online marketplaces like eBay or Alibaba.

Only industry metals traders have the bona fides required to sell to industry giants, guaranteeing market price sales.

All prices on this page last updated Jul 10 2026.