Weekly News Review October 21 – October 27 2024

October 27, 2024

Weekly News Review October 28 – November 3 2024

November 3, 2024

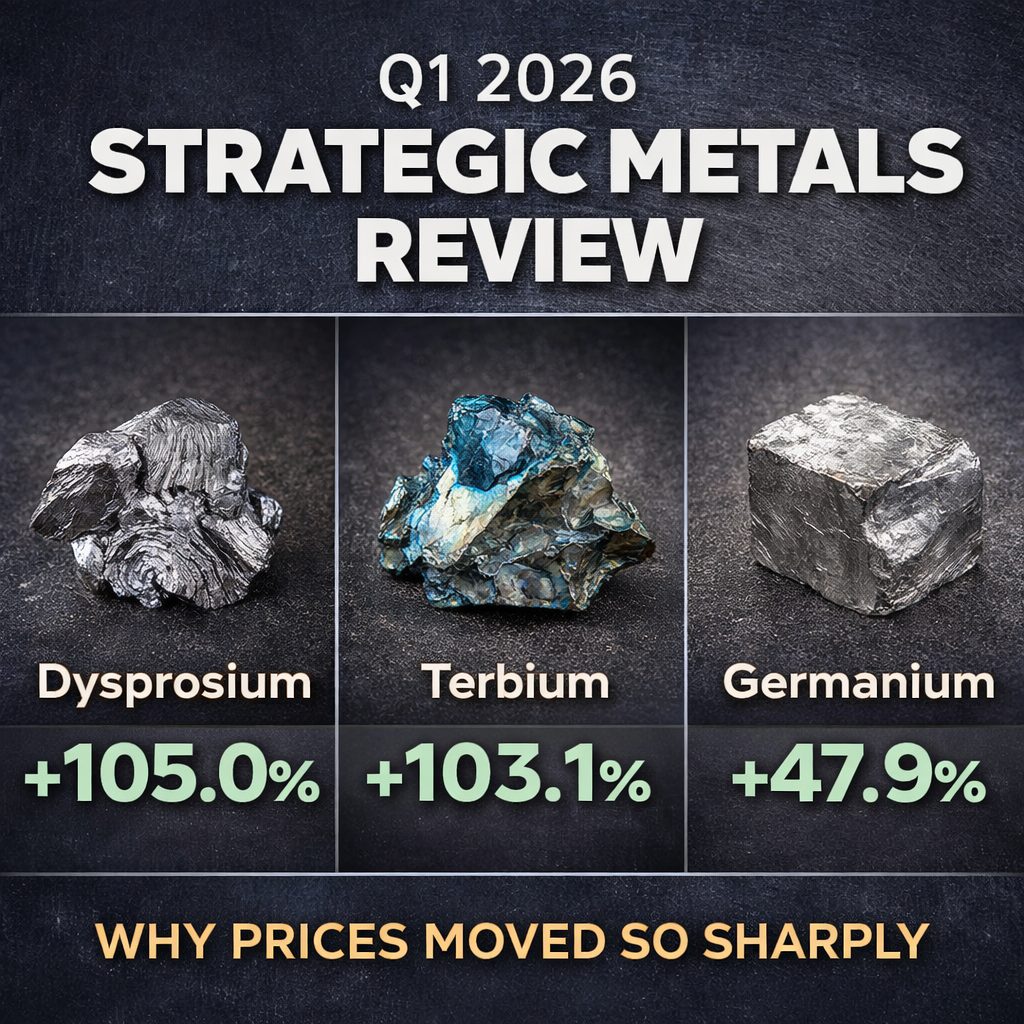

Most, if not all, price reporting agencies are predicting not only a shortage of rare earths and technology metals but also periods when there will simply not be enough to go around.

Suppose one takes the time to investigate online publishing portals like Argus Media, Fastmarkets, TARawmaterials, AsianMetal, etc. In that case, one will find the exact predictions for Gallium, Germanium, Indium, Rhenium, Indium, Dysprosium, Neodymium, Praseodymium, and Terbium.

The predictions are that prices will continue to rise, and invariably, there will be volatility, where the market can go from “quiet and steady” to crisis and then return to “quiet and steady” again. These are the periods when investors can profit most, and today, we will explain in detail how and why this happens and how and why it will continue until 2035 and beyond.

Here are two recent examples. Terbium was up 500% in three years recently and has now corrected. Hafnium went up 180% in one year right after COVID.

Like all good ideas, our offer is simple.

Increasing demand with limited supply = profit potential.

Let us start with demand.

Strategic Metals are the upstream materials that ultimately become trillions of dollars in downstream GDP. They are critical to all nations’ economic stability and military capabilities.

Would anybody argue that demand will not continue to increase for the raw materials critically needed for all modern technologies, including smartphones, computers, AI, superconductors, computer chips, electric cars, medical devices, aviation, solar power, the space industry, wind turbines, nuclear energy, cancer treatments, vehicle automation, robotics, and on and on?

The good news for private investors is that these metals are largely ignored by the “big money.” Despite being critical raw materials, they are largely under the radar of institutional money. The reason (s) is that the market is relatively small compared to gold and silver. Despite being critical to all nations’ economic prosperity, these metals have small economic visibility, and as we will now explain, production is challenging.

Again, the good news for private investors is that they can play this niche market and win. Here are some of the challenges for production and supply that will allow that to manifest.

- Rare Earths do not occur naturally in the earth’s crust. There are 17 rare earths, and they are all chemically similar, so they must be extracted, separated, and re-metallized to industrial-grade purity levels. This process is complicated, messy, and costly. China is a generation ahead of the rest of the world. Using Gallium as an example, 98% of the world’s Gallium is processed in China.

- There is an inelasticity to production. Rare Earths and technology metals are always a byproduct of the mining of another raw material. Gallium is a byproduct of aluminum mining. Hafnium is a byproduct of Zirconium mining. For example, for every 50 tons of Zirconium, there will be 1 ton of Hafnium. So, when demand for Hafnium increases, production is inflexible and cannot be ramped up. That is why Hafnium increased 180% in one year when the aviation industry returned from COVID-19—running parallel to space exploration becoming a fully-fledged space industry.

- Another critical factor is the “single point of failure”; this is a situation where a system is configured so that failure in one part of the system causes the entire system to fail. In manufacturing, all and any single points of failure must be identified and eliminated where possible, or risk managed when unavoidable. Because rare earths are critical to the iPhone, electric cars, and aviation industries, they represent a possible single point of failure for manufacturers, which means manufacturers will absorb any price increases rather than face the possibility of production shutdown.

- There are two ways manufacturers can mitigate against single points of failure. One is diversity in supply. This is not possible as China is the largest producer, importer, exporter, and user of these critical raw materials. China is the dominant market leader in rare earths and has been for some time. This war is over. China has won this one for now.

- The other alternative is a “cushion of inventory,” a buffer that can ensure operational continuity when supply is disrupted. This is ensuring that all raw materials are being purchased and either applied or stockpiled. The majority of “smaller” manufacturers who represent 80% of the global market cannot afford to stockpile and have nowhere to store anyway.

When this happens, investors holding these raw materials can and will profit. We invite you to participate safely in the supply chain and profit from increasing demand while supply is limited and subject to disruption.

If you want to learn more about adding strategic metals to your portfolio, please respond to this email.

{kind=link}

{kind=link}

{kind=link}