Strategic Metals Outlook 2026: From Supply Cycles to Geopolitics

February 13, 2026

Bismuth: Supply Structure, Export Controls, and the 2026 Outlook

February 19, 2026

Activity in critical minerals eased ahead of the Chinese Lunar New Year. Although next week’s celebrations will halt much of China’s industrial output, the quieter pre-holiday period still delivered several important developments.

METALS MINING DRIVES GROWTH IN US RAW MATERIALS SECTOR:

U.S. Geological Survey publishes annual Mineral Commodity Summaries.

The U.S. Geological Survey (USGS) has published its latest Mineral Commodity Summaries, highlighting strong growth in the U.S. raw materials sector in 2025, driven primarily by metals mining and higher commodity prices. Total nonfuel mineral production reached an estimated $112 billion, up from $106 billion in 2024. Metal production value rose by 13 percent to $38.1 billion, while industrial minerals increased modestly to $73.7 billion.

Battery and technology metals were among the most dynamic segments. U.S. production quantities for cobalt and nickel increased significantly. In contrast, lithium production volumes remained stable, but declining prices led to a drop in production value. Precious metals also contributed to growth: gold and silver prices climbed sharply, boosting production values despite only moderate changes in output.

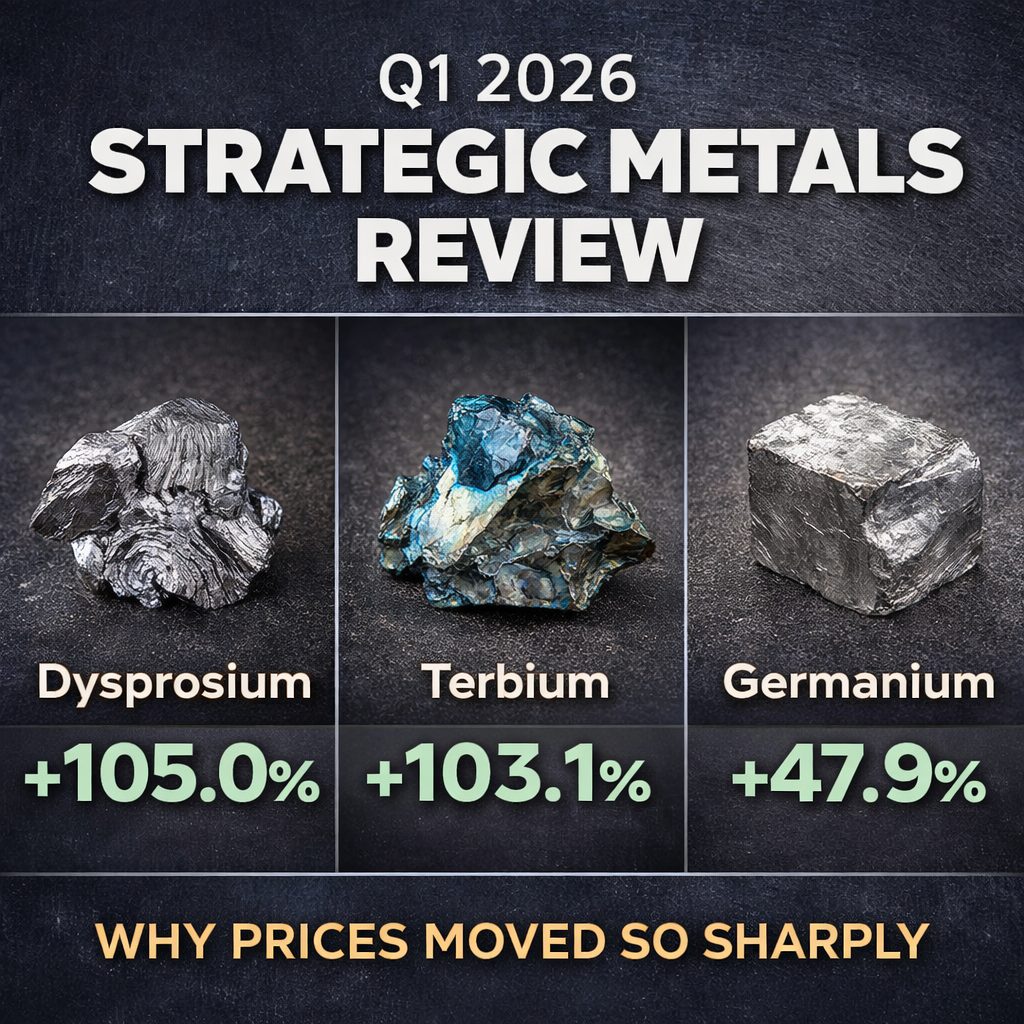

Commodity price trends were mixed overall. Global prices surged for specialty metals such as bismuth, antimony, and germanium, while lithium, manganese, and nickel prices declined. Domestic production volumes fell for several traditional metals, including palladium, platinum, iron ore, lead, and zinc, indicating ongoing structural adjustments within the mining sector.

The year also saw renewed investment in strategic mineral supply chains. Antimony mining resumed in the United States for the first time in decades, and rare earth processing capacity expanded across several states. Meanwhile, the iron and steel sector underwent restructuring, including mine idlings and new investment projects aimed at modernizing production.

The USGS also highlighted its recently updated 2025 Critical Minerals List, which now includes 60 commodities, underscoring the growing strategic importance of metals mining for U.S. industrial policy and supply security.

INDONESIA EYES RARE EARTHS:

Indonesia is already a global heavyweight in metal production, particularly in nickel and tin. The archipelago is also a significant producer of cobalt and now aims to enter the rare earths market. The country’s mining authority, BIM, expects that by 2030, processing these minerals domestically could generate nearly $7.5 billion in revenue.

BIM has identified eight exploration sites for rare earths and other critical minerals, and pilot processing projects are now set to begin. According to BIM head Brian Yuliarto, Indonesia has approached other countries for partnerships, but they prefer to buy the minerals directly rather than invest in developing local processing infrastructure.

Estimates of Indonesia’s rare earth reserves remain uncertain. In 2019, the national mining association reported that no exploration had been conducted to date and that the deposits were likely insignificant. Meanwhile, the geological agency estimates reserves between 118 and 650 tons of rare earth metals but emphasizes the need for detailed surveys.

TAIWAN EYES US RARE EARTHS TO FUEL DOMESTIC PROCESSING PLANS:

The Island nation plans to expand domestic processing capacities and is seeking feedstock material.

Taiwan plans to dispatch officials to the United States to evaluate rare-earth deposits, part of a broader strategy to secure critical minerals and strengthen its domestic supply chain, Economy Minister Kung Ming-hsin announced Wednesday, Reuters reported.

The assessment mission will be conducted by Taiwan’s Geological Survey and Mining Management Agency, focusing on identifying which rare earth elements are present and whether they meet Taiwan’s industrial needs. The island nation is home to one of the most sophisticated semiconductor industries in the world, where rare earths are used in wafer polishing or doped glass, for example. While Taiwan does not mine rare earths domestically, the island aims to refine imported materials, leveraging its advanced processing capabilities.

The trip comes after Taiwan announced earlier this month plans to build a pilot-scale rare-earth production line within three years. A scaled-up version would be capable of supplying about 50% of domestic demand, government officials said. The initiative has attracted strong interest from the United States, which is seeking to diversify its critical mineral supply chains away from China.

According to the U.S. Geological Survey, Taiwan’s domestic mineral resources are limited, with mining employing just about 1,000 people. The island has historically relied on imported ores, refined into steel, petroleum products, and other materials, making its processing sector far more significant than its extraction sector.

FINLAND INVESTS $65 MILLION IN EUROPE’S CRITICAL MINERALS INDEPENDENCE:

Sokli, a mineral deposit in Finland’s Lapland region, could help strengthen Europe’s critical minerals autonomy. According to the state-owned Finnish Minerals Group, which is developing the project, the phosphate reserves are particularly significant, potentially covering up to one-fifth of Europe’s demand. In addition, the deposit is estimated to contain substantial amounts of rare-earth elements, as well as other valuable minerals such as manganese, niobium, and copper.

The Finnish government now plans to accelerate the project with a €65 million investment. The funding will support a feasibility study for the potential production of phosphate and iron concentrates between 2027 and 2029. At the same time, the potential to extract additional minerals, including rare earths, will be assessed. The project also includes the construction of a pilot mine and a pilot processing plant.

Critical Raw Materials Act: Could Sokli Become a Strategic Project?

Sokli is also competing for designation as a strategic project under the EU’s Critical Raw Materials Act. Projects with this status can benefit from accelerated permitting processes and enhanced access to financing. Slow permitting is one reason Europe’s critical minerals independence is advancing only gradually; it can take years, or even decades, before new mines and processing facilities become operational.

Another factor that can delay, or even halt, projects is a lack of acceptance and engagement from local communities. Recent headlines highlighted protests against other Nordic deposits that were promoted as promising, including Norra Kärr and Per Geijer in Sweden. Against this backdrop, the Finnish Minerals Group emphasizes environmental responsibility: sensitive areas and natural waterways are to remain untouched, and the company is aiming for a climate-neutral value chain, including the use of renewable energy.

{kind=link}

{kind=link}