Weekly News Review March 23 – March 29 2026

March 29, 2026

Strategic metals did not stand still in the first quarter of 2026.

Across much of the market, rare earths and technology metals posted sharp gains, in some cases exceptionally sharp ones. More importantly, these moves were not confined to one or two obscure materials. The strength appeared across several strategically important metals, reinforcing a point that has become increasingly difficult to ignore: these are not markets driven mainly by investor sentiment or financial market fashion.

They are small, specialist industrial markets where prices can move decisively when supply remains concentrated, availability tightens, or governments interfere with trade.

In this Q1 2026 strategic metals review, we look at which metals moved most, what likely drove those gains, and why the broader backdrop heading into Q2 deserves close attention.

Q1 2026 performance snapshot

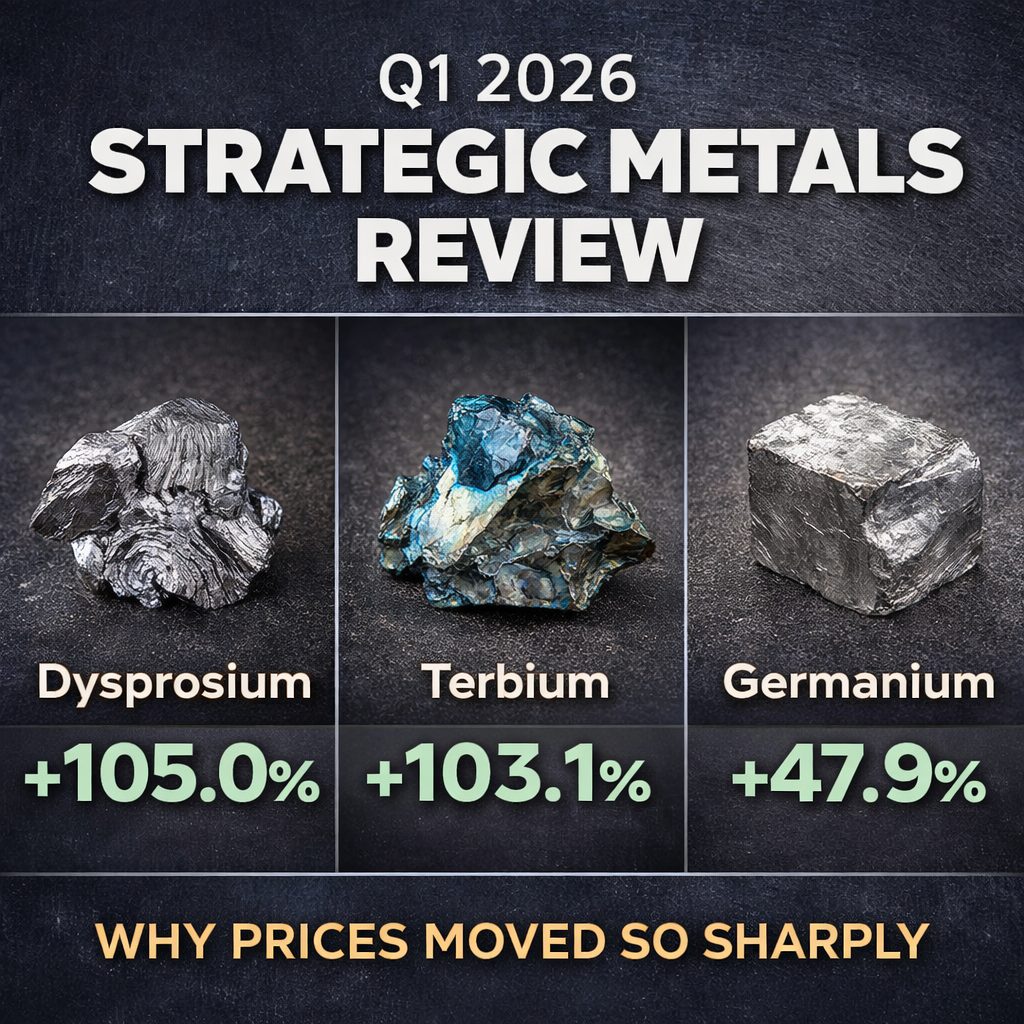

Core strategic metals

| Metal | Price 31 Mar 2026 | Q1 2026 |

|---|---|---|

| Dysprosium | $930.70/kg | +105.0% |

| Terbium | $4,028.50/kg | +103.1% |

| Germanium | $8,597.50/kg | +47.9% |

| Praseodymium | $212.60/kg | +47.5% |

| Neodymium | $218.80/kg | +46.6% |

| Rhenium | $6,389.30/kg | +34.2% |

| Gallium | $2,269.40/kg | +31.7% |

| Hafnium | $12,508.20/kg | +31.7% |

| Indium | $972.20/kg | +16.7% |

Additional metals added for 2026

| Metal | Price 31 Mar 2026 | Q1 2026 |

|---|---|---|

| Bismuth | $65.40/kg | +19.1% |

| Tellurium | $221.70/kg | +1.0% |

| Antimony | $49.10/kg | -10.8% |

Price changes shown from the last published 2025 price to March 31, 2026.

Why did strategic metals rise so sharply in Q1 2026?

The short answer is that Q1 continued a trend that has been building for some time: strategic metals are increasingly being shaped by policy and availability, not just by ordinary price cycles.

That distinction matters.

Unlike exchange-traded commodities, many strategic metals sit inside opaque industrial supply chains. Supply is often concentrated, production volumes are small, and several of these materials are produced only as by-products of other mining or refining processes. That means supply cannot always respond quickly when demand rises or when export restrictions disrupt the market.

In practice, this creates exactly the kind of setup in which sharp repricing can occur.

Rare earths led the way

The most dramatic Q1 moves came from the rare earths, especially dysprosium and terbium.

Both metals are closely associated with high-performance magnets and applications where thermal stability and specialised performance matter. When supply chains are fragile and geopolitical pressure is high, these markets can move quickly because they are relatively small and difficult to rebalance.

Neodymium and praseodymium also posted very strong gains. That suggests the quarter was not just about the tightest corners of the rare earth market. It points to broader firmness across the magnet metals complex as a whole.

This is one of the more important takeaways from Q1: the move was not isolated. It was broad enough to suggest that strategic importance, concentrated supply, and industrial relevance are continuing to assert themselves across multiple rare earth markets.

Technology metals also posted strong gains

The technology metals told a similar story.

Germanium, gallium, hafnium, and rhenium all recorded strong first-quarter gains. These are not random materials. Each is tied to sectors that have become strategically important in their own right, including semiconductors, aerospace, defence, communications, and advanced manufacturing.

That matters because it reinforces the wider point behind investing in strategic metals: these are physical materials embedded in real industrial systems. Their value is linked to necessity, not fashion.

Even the more moderate gainers, such as indium and bismuth, still fit the same broader pattern of structurally sensitive supply. Tellurium was comparatively quiet, while antimony moved lower, which is a useful reminder that these are not one-way markets. Different supply structures, different policy pressures, and different industrial uses can produce very different outcomes even within the same quarter.

The bigger takeaway from Q1 2026

What Q1 showed is that strategic metals remain a market where scarcity, relevance, and policy can collide at once.

That is also why this asset class is best viewed through a long-term lens.

These materials sit inside the infrastructure of the modern world: electrification, energy systems, electronics, aerospace, communications, and defence. Yet many are still produced in small volumes, often as by-products, and still rely heavily on highly concentrated supply chains.

That combination does not guarantee smooth price appreciation. Strategic metals can be volatile, uneven, and highly metal-specific.

But it does create conditions where price adjustments can be sudden and where access itself can become part of the story.

For private investors, that is one of the defining differences between strategic metals and more familiar assets. These are not paper exposures to broad commodity indices. They are specialist physical materials whose markets are shaped by industrial necessity and supply fragility.

What to watch in Q2 2026

As Q2 begins, investors will be watching whether the forces that drove Q1 remain in place or intensify.

The quarter closed against a rapidly changing geopolitical backdrop. Even where recent events do not fully explain the strongest Q1 price moves, they may still become highly relevant in Q2 if energy markets, transport routes, and industrial input costs come under fresh pressure.

That is why the next phase may matter just as much as the last one.

The key question is no longer simply which metals moved in Q1. It is which markets remain most exposed to further supply tension, policy intervention, or industrial bottlenecks as 2026 continues.

Final thoughts

Q1 2026 was a powerful reminder that strategic metals remain one of the most unusual corners of the tangible asset world.

They are not conventional commodities. They are not driven mainly by broad financial flows. And they do not need mainstream attention to move sharply.

They simply need tight supply, real industrial demand, and a policy environment that adds further pressure to already fragile markets.

That combination was clearly visible in the first quarter of 2026, and it may remain highly relevant in the months ahead.

The strongest Q1 2026 performers were dysprosium and terbium, both of which rose by more than 100%. Germanium, praseodymium, and neodymium also posted strong gains.

Strategic metals rose because many of these markets remain small, supply-constrained, and highly sensitive to policy decisions, export controls, and industrial demand shifts.

Germanium, gallium, hafnium, and rhenium were among the strongest-performing technology metals in Q1 2026.

No. Most strategic metals are not traded on public exchanges. They are specialist industrial materials bought and sold through industrial supply chains.

They are essential for semiconductors, electrification, renewable energy, aerospace, defence systems, and advanced manufacturing.

{kind=link}

{kind=link}

{kind=link}