Weekly News Review March 30 – April 5 2026

April 5, 2026

With the first quarter of 2026 behind us, the next question is not simply whether strategic metals can keep moving higher.

It is which parts of this market remain most exposed to supply tension, export controls, and rising strategic demand.

That matters because these are not markets driven mainly by investor flows or broad commodity sentiment. Strategic metals are small, specialised industrial markets. When supply becomes constrained, or governments decide access matters more than price, the adjustment can be fast and severe. That is exactly why Q2 deserves close attention.

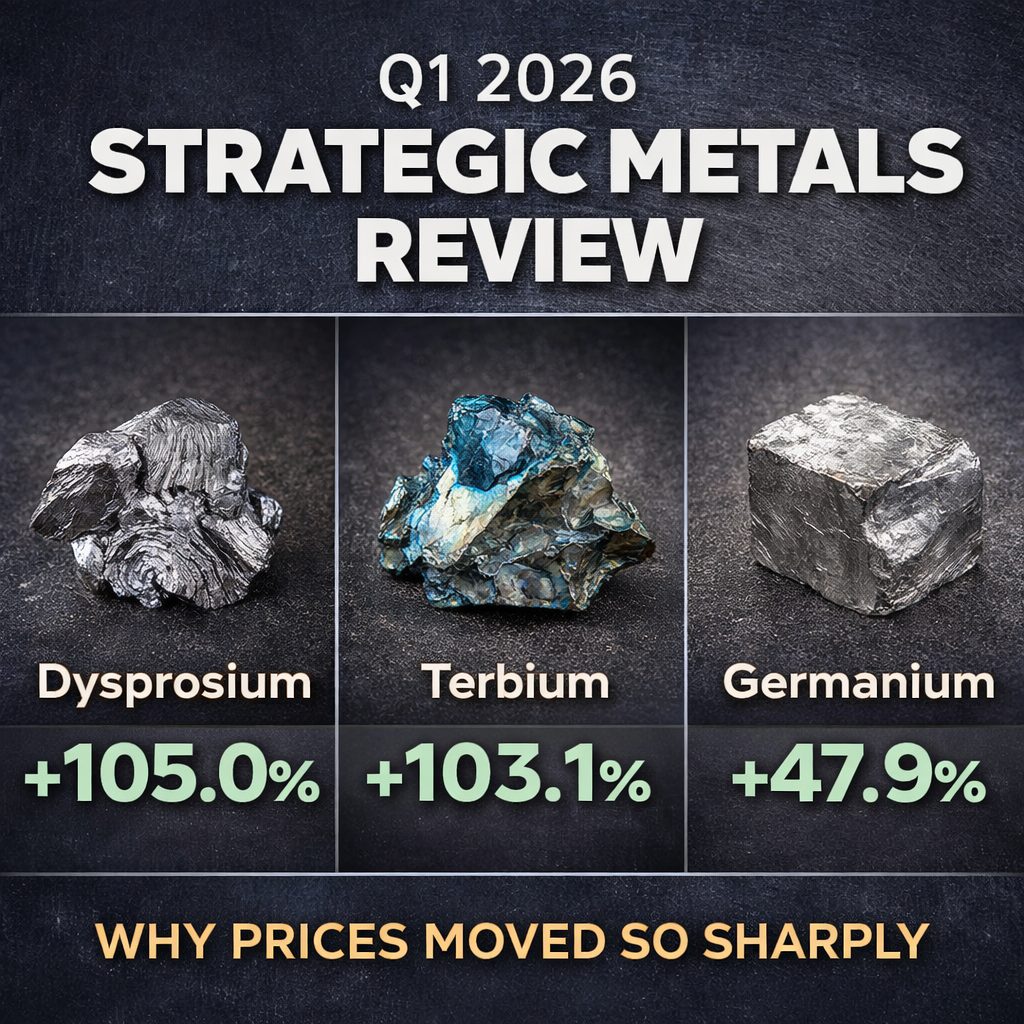

Heavy rare earths still look like the key pressure point

If one group of metals continues to stand out, it is the heavy rare earths, especially dysprosium and terbium.

Recent industry reporting points to a sharp decline in dysprosium and terbium exports at the start of 2026, with stricter approval procedures in China playing an important role. That matters because these are already highly sensitive markets with limited supply flexibility. When approvals slow, availability tightens quickly.

These metals sit at the high-value end of the magnet supply chain. They are used to improve heat resistance and performance in permanent magnets, which remain critical for electric motors, wind turbines, and a range of defence-related applications. At the same time, Western groups are still working to build alternative heavy rare earth capacity, including new processing efforts in France. That underlines the broader point: supply diversification is being pursued, but it is still a work in progress.

In practical terms, this means dysprosium and terbium remain among the metals most vulnerable to further supply tension in Q2.

Neodymium and praseodymium should not be ignored

Heavy rare earths may be the most visibly constrained, but the broader magnet metals complex also deserves attention.

Chinese rare-earth magnet exports rose 8.2% year on year in January and February 2026, yet shipments to the United States fell 22.5% over the same period. That divergence is a reminder that even when volumes look healthy at the aggregate level, access is becoming increasingly political and selective.

That matters for neodymium and praseodymium because both sit at the centre of permanent magnet production. If governments continue to prioritise secure supply chains, and if strategic sourcing rather than just spot availability becomes the dominant theme, the wider magnet metals complex could remain firmly in focus throughout Q2.

Gallium and germanium remain access stories, not just price stories

Gallium and germanium are still two of the clearest examples of why strategic metals behave differently from mainstream commodities.

Recent industry reporting highlights that gallium and germanium trade flows are becoming more concentrated, with shipments increasingly directed toward a limited number of recipient countries while some markets, including Japan, are receiving very little supply. That is exactly the kind of development that keeps these metals strategically important even when prices are not making daily headlines.

The real issue here is not just what the quoted price happens to be on a given day. It is whether industrial buyers can secure reliable material at all, and under what conditions. In markets tied to semiconductors, fibre optics, communications, and defence technologies, availability often matters more than short-term price volatility. That remains true in Q2.

Hafnium and rhenium remain quieter but important

Not every meaningful market move comes from the metals making the biggest headlines.

Hafnium and rhenium remain particularly interesting because both sit in very small industrial markets where supply is difficult to expand and substitution is limited. Hafnium continues to matter in semiconductors, aerospace, and nuclear applications, while rhenium remains closely tied to turbine alloys and other high-performance aerospace uses. These are not broad, liquid commodity markets. They are specialised industrial supply chains where even modest changes in procurement or availability can have an outsized impact. That is part of what makes them worth monitoring in Q2.

Governments are now part of the market

One of the clearest lessons from the past year is that strategic metals are increasingly being shaped by policy, not just industrial demand.

In February 2026, the United States proposed a critical minerals trade bloc with allies, with 55 countries attending talks in Washington. The initiative included discussion of price floors, standards, subsidies, and guaranteed purchases to encourage non-Chinese production. Around the same time, Japan, France, and Canada were also reported to be working on alternative frameworks to secure rare earth supply and reduce dependence on China.

This is significant because it confirms that strategic metals are no longer just a procurement issue for manufacturers. They are now a policy issue for governments. Once that happens, markets can stop behaving like ordinary commodity markets and start behaving like strategic bottlenecks.

The bigger takeaway for Q2

Q1 2026 reminded investors that strategic metals can move sharply when supply tightens. Q2 may now reinforce a second lesson: in these markets, the story often begins with access, approvals, and geopolitics long before it shows up fully in the price chart.

For that reason, heavy rare earths still look like the most obvious pressure point. But they are not the only one. Neodymium and praseodymium remain central to the magnet story. Gallium and germanium remain deeply tied to export controls and licensing risk. Hafnium and rhenium continue to sit in structurally tight, specialised markets. And governments across the US, Europe, and allied economies are becoming more directly involved in how these supply chains are built.

That does not mean every metal will move the same way, or on the same timetable.

It does mean strategic metals remain one of the few asset classes where industrial necessity, concentrated supply, and government action can all collide at once.

And that is exactly why they continue to deserve close attention.

{kind=link}

{kind=link}

{kind=link}