Q2 2026 Strategic Metals Outlook: What Investors Should Watch

April 10, 2026

What is the cost of diversifying rare earth supply chains? The International Energy Agency has presented new estimates, while U.S. companies are already taking concrete steps. Read the full details in our roundup.

THE UNITED STATES AND JAPAN RAMP UP THE RACE FOR CRITICAL RAW MATERIALS:

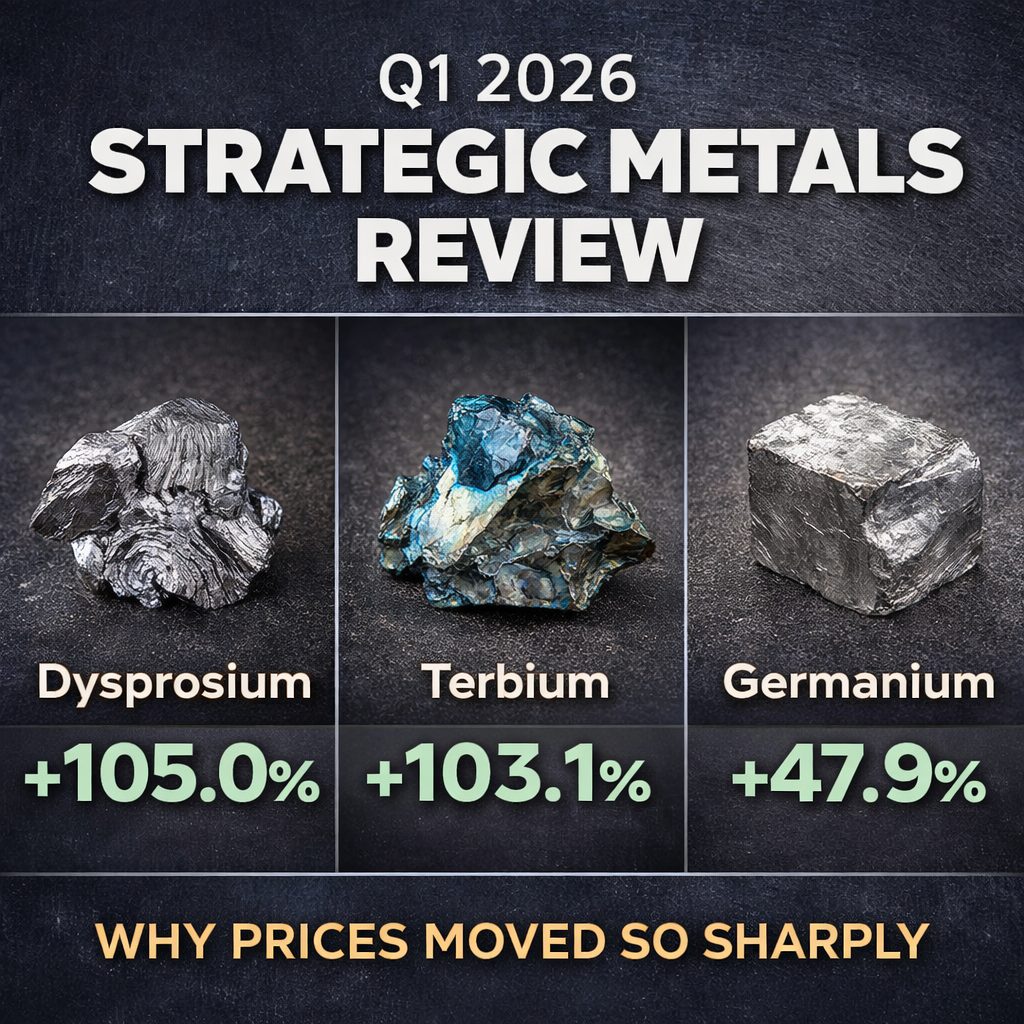

Export restrictions, newly imposed price ceilings, and the formation of strategic raw material alliances continued to shape market dynamics in the first quarter of 2026. The trends observed in the previous year persisted with notable consistency. In collaboration with our raw materials trading company TRADIUM GmbH, the key developments in the United States, China, and Europe were analyzed, and their implications for global commodity markets were assessed.

You can download the report here.

IEA: $60 BILLION NEEDED TO REDUCE DEPENDENCE ON CHINA FOR RARE EARTHS:

The International Energy Agency (IEA) published a new report on Wednesday addressing supply security for rare earth elements. The analysis covers all stages of the value chain, from extraction to processing, and highlights the risks associated with potential supply chain disruptions. In particular, the supply of those rare earth elements used in magnet applications is heavily concentrated in a small number of countries. China holds a quasi-monopoly in this segment.

Rare earths such as Neodymium and Terbium are also used in other technologies; however, according to the IEA, permanent magnets account for 95% of total rare earth consumption. Export restrictions imposed by Beijing last year have clearly demonstrated the potential and actual consequences of supply disruptions, the report adds.

To diversify the supply of rare earths and significantly reduce dependence on China, investments totaling $60 billion from both private and public sources will be required over the next decade, the authors state.

The majority of this capital will need to be directed toward processing, with roughly one-third allocated to manufacturing. While this investment requirement may initially appear substantial, it is negligible compared to the potential costs of supply disruptions, which the IEA estimates at $6.5 trillion.

USA: DEPARTMENT OF ENERGY TO SUPPORT DOMESTIC PRODUCTION OF CRITICAL RAW MATERIALS –

The United States is continuing to expand its raw materials strategy: the U.S. Department of Energy (DOE) announced this week two new programs, the Critical Minerals and Materials Accelerator and an additional funding initiative totaling up to $69 million, aimed at accelerating innovative technologies across the critical minerals value chain toward commercial deployment.

The focus is particularly on the extraction, processing, and refinement of strategically important materials, including rare earth elements, gallium, germanium, and lithium, as well as recovery from unconventional sources such as geothermal systems. Industry-led projects will receive targeted support to bridge the gap between laboratory-scale innovation and industrial-scale application.

The objective of these measures is to close existing gaps in the U.S. critical minerals supply chain, reduce reliance on foreign imports, and strengthen long-term supply security and economic competitiveness. In the refining and downstream processing sector, China currently holds a dominant position in global markets.

USA RARE EARTH SECURES ACCESS TO KEY TECHNOLOGIES IN EUROPE:

Is France becoming a model for the rare earth industry?

USA Rare Earth is expanding its expertise: following the acquisition of the British metals and alloys producer Less Common Metals, the company is now shifting its focus toward the separation, processing, and recycling of rare earth elements. To this end, the U.S. firm has acquired a 12.5 percent stake in Carester, a company based in Lyon, France, as announced on Thursday.

In addition to gaining access to technical know-how, USA Rare Earth will have the right to purchase part of Carester’s oxide production. In turn, the French company could benefit from access to heavy rare earth elements, which USA Rare Earth plans to begin producing in the United States by the end of 2028. At present, China dominates this segment.

The transaction is part of a broader initiative by USA Rare Earth, Less Common Metals, and Carester to establish an industrial platform spanning the entire rare-earth value chain, from processing to magnet manufacturing. This platform is to be located in the French département of Pyrénées-Atlantiques.

Carester had already presented plans for such a facility in March of last year, with financial support pledged by the French government.

The site will now be complemented by a metals and alloys plant, which may also receive state backing. According to the companies involved, this would create the most comprehensive rare earth industrial ecosystem in Europe.

FIGURE OF THE WEEK: – MORE THAN $1.5 TRILLION – ACCORDING TO THE IEA, THIS IS THE SCALE TO EUROPE AND THE UNITED STATES IF DISRUPRTIONS TO RARE EARTH SUPPLIES WERE TO OCCUR.

{kind=link}

{kind=link}

{kind=link}