Weekly News Review April 13 – April 19 2026

April 19, 2026

Weekly News Review April 27 – May 3 2026

May 3, 2026

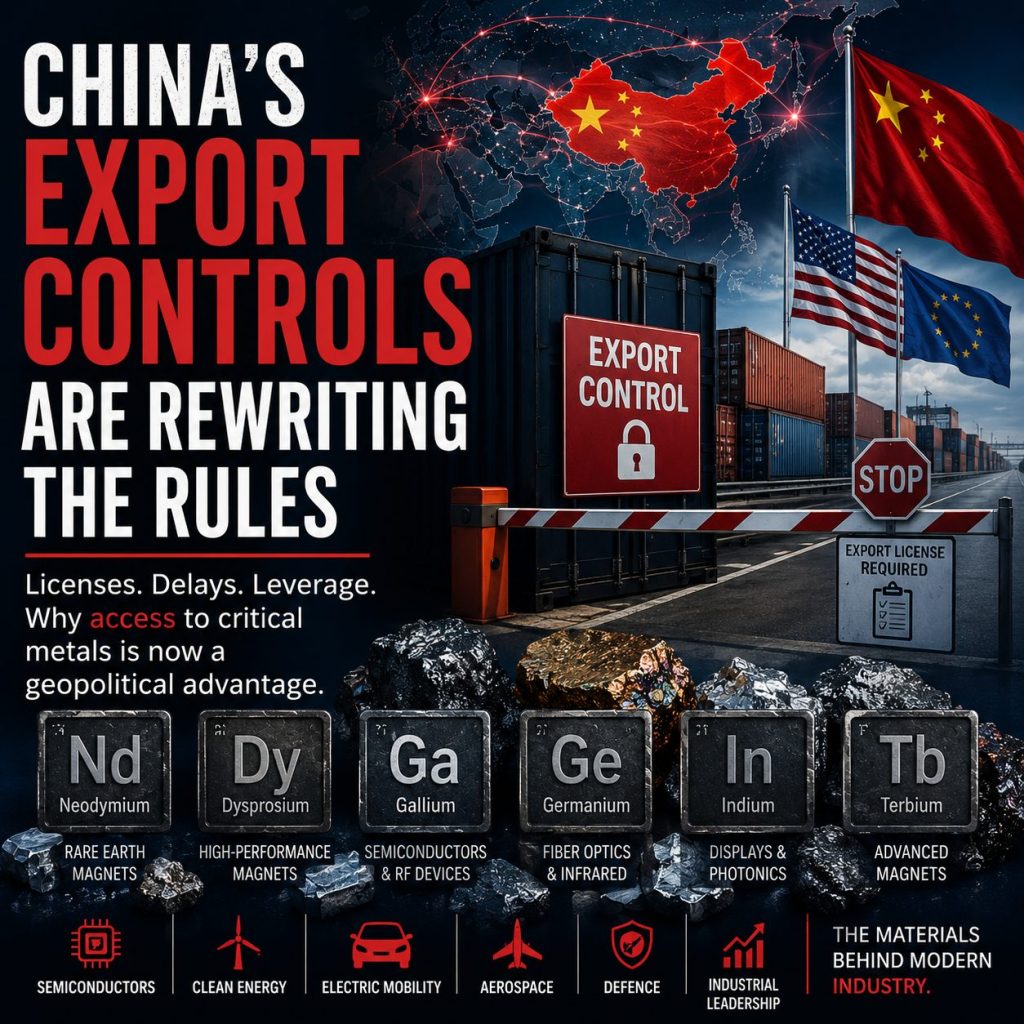

Beijing’s trade restrictions on critical raw materials are affecting exports, as recent foreign trade statistics show. The US Trade Representative also recently reminded audiences that building a counterweight to the raw materials superpower will come at a cost. However, calendar week 17 had much more to offer — to find out what exactly, read our roundup.

CHINA INCREASES EXPORTS OF RARE EARTH MAGNETS:

China’s exports of rare earth magnets rose by more than ten percent in March compared to the previous month of February. At 5,238 tonnes, export volumes were roughly in line with the level seen in the same period last year. By far the largest recipient was Germany, followed by South Korea, Vietnam, the United States, and India. As in February, Japan also ranked among the top ten destinations.

CHINA: TERBIUM EXPORTS REMAIN AT A LOW LEVEL –

After no dysprosium was exported from China in February, the latest customs data for March show an increase to 7,386 kilograms, moving back toward last year’s level. The majority of the material was shipped to South Korea, while Portugal received a smaller volume.

For terbium, the decline seen in February continues: only three kilograms were exported, all of which went to Australia. Since April 2025, China has imposed strict export controls on dysprosium, terbium, and other rare earth elements. For comparison, nearly 11 tonnes of terbium were shipped in March 2025, shortly before the measures took effect.

Dysprosium and terbium enhance the performance of permanent magnets, particularly at high temperatures. China dominates the production of both materials.

GALLIUM AND GERMANIUM: CHINA’S EXPORTS REMAIN HIGHLY CONCENTRATED –

In March, only a few countries, such as Russia and Germany, received shipments of these critical raw materials. For germanium, export volumes rose sharply compared to the previous month.

China’s exports of the critical raw material gallium remain highly concentrated. This is shown by the latest data from the country’s customs authorities.

At 5,000 kilograms, the lion’s share of the material was shipped to Germany in March. In the two previous months, Germany had been the only buyer of gallium. In March, South Korea received an additional 120 kilograms, and Malaysia received 200 kilograms.

Japan—China’s largest importer of gallium in 2025—remains cut off from supplies, likely due to tightened export controls targeting the country.

While there was little change in the list of recipient countries, the total export volume of 5,320 kilograms was roughly in line with January (5,000 kilograms) and February (6,000 kilograms). In December, however, the volume had been significantly higher at 10,809 kilograms.

Germanium Exports Rise Sharply:

In contrast, germanium exports rose by more than 35 percent in March to just under 1,000 kilograms, compared with the previous month (736 kilograms). However, the volume remains well below the figure of nearly 1,500 kilograms recorded a year earlier.

As with gallium, supply flows are concentrated. Russia remained the main recipient in March, receiving 600 kilograms, the same as in February. The only other countries receiving notable amounts were Germany, with 276 kilograms, and Turkey, with 117 kilograms.

Both gallium and germanium are essential for numerous civilian and military applications, including semiconductor production. China imposed strict export controls on these materials in the summer of 2023. Since then, trade flows have fluctuated significantly and, in some cases, depend on political relations with the respective recipient countries.

USA RARE EARTH ACQUIRES BRAZILIAN RARE EARTH PRODUCER:

USA Rare Earth (USAR) is acquiring Serra Verde, a Brazilian rare earths producer, the company announced on Monday (PDF), valuing the transaction at $2.8 billion.

CEO Barbara Humpton described the move as a key step toward building a global market leader. Serra Verde’s Pela Ema mine is the only operation outside Asia capable of supplying the magnet materials neodymium, praseodymium, terbium, and dysprosium at scale, she said.

At the same time, a 15-year supply agreement has been signed with a special purpose vehicle backed by the U.S. government and private investors. According to USAR, the contract includes minimum price guarantees for the four rare earth elements. Such mechanisms have recently been discussed and, in some cases, implemented by Western countries to improve the competitiveness of non-Chinese producers.

The acquisition marks the latest step in USAR’s strategy to build a complete value chain. The company plans to mine rare earths at its Texas deposit and manufacture rare earth magnets. To cover the intermediate steps, USAR acquired Less Common Metals last autumn, one of the few producers of rare earth metals and alloys outside China. More recently, the company also took a stake in the French firm Carester, which specializes in rare earth separation and recycling.

Earlier this year, the U.S. government invested in USAR and supported its plans to expand the value chain. Shortly thereafter, Serra Verde also received funding from the U.S. International Development Finance Corporation.

AUSTRALIA: LYNAS SIGNIFICANTLY INCREASES REVENUE –

Rare earths producer benefits from strong demand and higher prices.

Lynas reported (PDF) a significant increase in revenue for the third quarter of fiscal year 2026 (January to March), reaching USD 190 million. This represents a 115 percent increase compared to the same period last year. For the reporting period, the rare earths group recorded production of 1,996 tonnes of NdPr (neodymium-praseodymium) as well as eight tonnes of the heavy rare earths dysprosium and terbium. The separation of these two elements is still largely dominated by China, with Lynas increasingly positioning itself as an alternative supplier.

The company attributed the positive quarterly performance to both higher NdPr prices and increased sales volumes. Demand remains strong as companies and governments continue to build independent rare-earth supply chains outside China to reduce geopolitical risks and secure critical industries.

In addition, Lynas is strengthening its market position through long-term supply agreements with partners in Japan and the United States, as well as expanding its value chain in metal processing.

TRACEABILITY AIMS TO REDUCE RAW MATERIALS RISKS – IMPLEMENTATION STILL LAGS BEHIND:

An IEA and OECD report shows progress, but ongoing barriers include high costs and a lack of international standards. Structural challenges, particularly in rare earth supply chains, slow adoption.

New export restrictions from China and rising geopolitical tensions have once again highlighted supply risks in critical raw materials over the past year. While supply chains—especially in processing and refining—remain highly concentrated and demand for lithium, rare earths, and other materials continues to grow, the development of alternative sourcing options is struggling to keep pace. This is according to a new report by the International Energy Agency (IEA) and the OECD.

In recent years, a wide range of policy measures has been introduced to reduce these risks. In strategies focused on diversifying supply chains and promoting sustainable, responsible sourcing, traceability systems play a central role. A joint survey by the IEA and OECD of more than 80 companies shows that around two-thirds already use such systems. Upstream actors are significantly more advanced than those in midstream and downstream segments. Traceability systems are most widespread in cobalt supply chains.

In rare earths, there is a strong interest, but implementation is hindered by structural challenges. These include the very small quantities of these materials used in components, generic or inconsistent labeling, and concerns over protecting trade secrets.

Expanding Traceability Could Reduce Investment Risks:

The survey also shows that many systems remain incomplete. While nearly all companies collect country-of-origin data, more detailed information—such as environmental impact or corporate responsibility data—is far less commonly gathered. Yet such data could help attract investment and reduce risk, particularly in early-stage, less standardized supply chains such as those for graphite, rare earths, and lithium.

The authors identify high costs, lack of interoperability between systems, and weak incentives for data sharing as key barriers to further expansion. They recommend targeted financial support for upstream and smaller actors in particular. In addition, international standards should be better aligned to make data more comparable and easier to use.

USA: PRICE PREMIUM ON NON-CHINA RARE EARTHS UNAVOIDABLE, SAYS US TRADE OFFICIAL JAMIESON GREER –

A proposed minerals club is intended to serve as a counterweight to China.

China dominates the production of numerous critical raw materials, giving it significant leverage over global pricing and supply chains. According to the Financial Times (Paywall), quoting U.S. Trade Representative Jamieson Greer, countries seeking to diversify their supply chains would have to be willing to pay a premium for materials sourced outside China.

Greer is reportedly working on proposals for a coalition of allied countries — a so-called “raw materials club” — that would set minimum prices for critical minerals in order to reduce dependence on China and build more stable, geopolitically secure supply chains.

The U.S. first began discussions on such an initiative with G7 and European Union representatives last September. However, according to the Financial Times, potential participant countries are concerned about rising costs for industry and consumers, additional inflationary pressure, and possible retaliatory measures from China that could further strain global trade.

The concept of a coordinated market for raw materials sourced from friendly nations is not entirely new. The Biden administration previously advocated for similar frameworks, and the European Commission floated a comparable idea in 2022, partly in response to industrial subsidies under the U.S. Inflation Reduction Act.

{kind=link}

{kind=link}