Weekly News Review June 8 – June 14 2026

June 14, 2026

Weekly News Review June 15 – June 21 2026

June 22, 2026

For years, the world worried about where critical minerals were mined.

That was only half the story.

The more important question is now becoming painfully obvious: who controls the processing, the paperwork, the export licences, and the final permission slip?

Because in the world of strategic metals, a mine is not enough. You can have the geology, the ambition, the press release, and the ribbon-cutting ceremony. But if you do not have refining capacity, specialist processing, technical know-how, industrial relationships, and export approval, you may still be standing outside the factory gates holding a very impressive shovel.

China understood this long before most of the West did.

While Western economies spent decades outsourcing the messy and complicated parts of the raw materials chain, China built dominance not only in mining, but in refining, separation, magnet production, and the industrial networks that sit between the ground and the finished product.

Now, that position is being used with increasing precision.

Not always as a hammer. Sometimes as a valve.

And that may be even more powerful.

The new weapon is not always a ban

When people hear “export controls”, they often imagine a dramatic embargo. Ships stopped. Borders closed. Headlines flashing red.

But modern export controls are often subtler than that.

They can involve licensing requirements, end-user checks, customs reviews, documentation delays, product-specific restrictions, and political discretion. They do not necessarily shut the door. They simply make the doorway narrower, slower, and more unpredictable.

For industrial buyers, that can be enough.

If you manufacture semiconductors, electric motors, aerospace components, defence systems, or advanced electronics, you do not build your business around “maybe”. You need reliable supply. You need qualified materials. You need certainty that next month’s shipment will arrive on time and meet specification.

A delayed licence can be just as disruptive as a higher price.

A missing approval can hold up production.

A vague policy signal can force companies to rethink entire supply chains.

This is why China’s export controls matter so much. They are not simply about restricting a metal today. They are about reminding the world who controls access tomorrow.

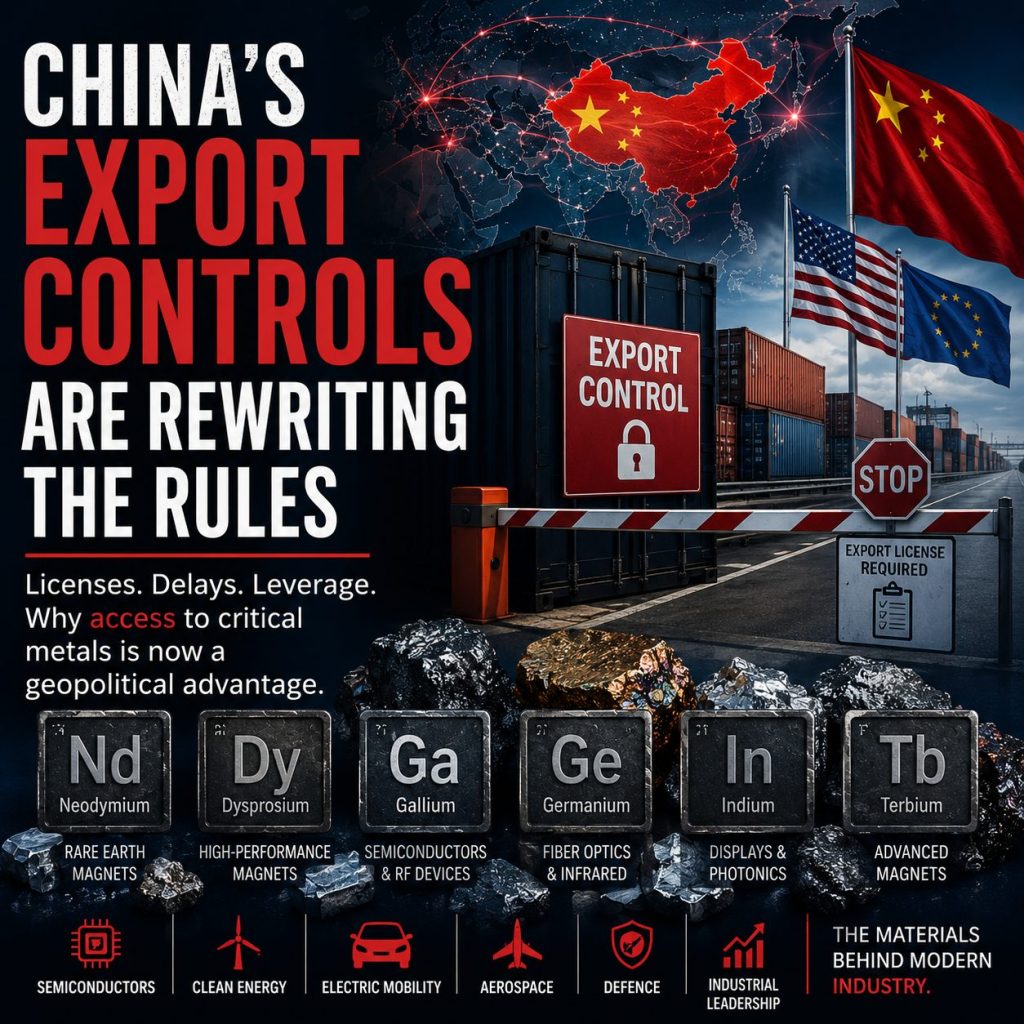

Rare earths: the magnet problem

Rare earths are a perfect example.

The world wants more electric vehicles, more wind turbines, more robotics, more drones, more automation, and more advanced defence systems. Many of those technologies rely on high-performance permanent magnets.

Those magnets, in turn, rely on rare earth elements such as neodymium, praseodymium, dysprosium, and terbium.

Neodymium and praseodymium provide magnetic strength. Dysprosium and terbium help magnets perform under high temperatures and demanding conditions. This matters in electric motors, wind turbines, aerospace systems, and defence applications, where reliability is not a luxury feature.

The problem is not simply that China mines rare earths.

The bigger issue is that China dominates the refining, separation, and magnet-making ecosystem. That gives Beijing influence over the most technically important parts of the supply chain.

In 2025, China introduced export controls on several medium and heavy rare earth-related items, including terbium and dysprosium materials. Later in the year, a further tightening of controls was temporarily suspended after high-level diplomacy.

That pause was welcomed by industry, of course. Nobody complains when the pressure valve is turned back slightly.

But a pause is not the same as peace.

The underlying framework remains. The political leverage remains. The dependency remains.

And for companies trying to plan multi-year production cycles, that is the part that matters.

Gallium and germanium: the semiconductor warning shot

Gallium and germanium have become the textbook case of how obscure technology metals can suddenly become geopolitical celebrities.

These are not household names. They do not appear in jewellery shop windows or central bank vault reports. Yet they are deeply embedded in the technologies that modern economies are desperate to control.

Gallium is used in advanced semiconductors, power electronics, LEDs, radio-frequency components, and solar technologies.

Germanium is important for fibre optics, infrared optics, high-performance electronics, and defence-related systems.

In other words, these are small metals with large strategic shadows.

China’s controls on gallium and germanium showed Western manufacturers how vulnerable specialised supply chains can be. The issue was not simply whether material existed somewhere in the world. The issue was whether properly refined, industrially qualified material could be sourced reliably, at scale, and without political friction.

That is a much tougher question.

A technology company cannot simply replace a missing supply chain by ordering “some gallium” from somewhere else. Qualification takes time. Alternative refining capacity takes years. Industrial users need consistency, purity, documentation, and reliability.

The metal may be tiny. The bottleneck is not.

Indium enters the AI conversation

The same theme is now appearing in the AI supply chain.

Indium phosphide, a compound used in advanced optical chips and photonics, has become a growing concern for AI data-centre development. Photonics is increasingly important because data centres need faster and more energy-efficient ways to move information than traditional copper connections can provide.

Once again, the issue is not the glamour of the finished technology. It is the quiet upstream material that allows the glamour to function.

AI may be sold with images of glowing servers and futuristic intelligence. But behind the curtain sit wafers, substrates, compounds, refiners, permits, and export licences.

The digital world has a very physical supply chain.

That is the point investors should not miss.

The West is responding, but slowly

The response from Western governments has been energetic, but uneven.

The G7 is working to reduce dependence on single suppliers for critical minerals and is discussing coordinated stockpiling, market monitoring, recycling, and investment support. Canada and South Korea are developing plans for joint critical-minerals stockpiling. The European Union is trying to accelerate domestic and allied supply through its Critical Raw Materials framework.

These are serious developments.

But building alternative supply chains is not like switching mobile phone providers.

New mines take years. Refineries take years. Permitting takes years. Customer qualification takes years. Environmental approvals, financing, infrastructure, technical talent, and political support all need to line up.

And even then, the hardest part is often not mining the material. It is processing it to the exact standard industry needs.

This is where China’s advantage remains formidable. It built the middle of the supply chain while others focused on either the mine or the finished product.

That middle is where much of the power now sits.

Why this matters for private investors

For private investors, the lesson is not that every export control automatically creates an investment opportunity. Markets are more complicated than that, and strategic metals should never be treated as short-term trading chips.

The real lesson is structural.

Strategic metals are no longer just industrial inputs. They are becoming instruments of policy, leverage, and national resilience. Their value is shaped not only by supply and demand, but by access, regulation, geopolitics, and the ability of manufacturers to secure qualified material when they need it.

That makes them very different from traditional commodities.

Gold is valued partly because it has no industrial permission slip. Strategic metals are valuable precisely because industry needs them and access is difficult.

This is why physical ownership deserves attention.

Properly sourced and professionally stored strategic metals offer exposure to real materials sitting at the heart of modern industry. They are not financial abstractions. They are not a bet on a mining company’s management team. They are not a derivative of a derivative wrapped in a nice factsheet.

They are physical assets.

And in a world where supply chains are becoming more political, that physical reality matters.

The new rules

The old raw materials model was simple enough: mine, refine, ship, manufacture.

The new model is more complicated: mine, refine, license, approve, verify, ship, monitor, restrict, renegotiate, diversify, stockpile, and hope nobody changes the rules next quarter.

That is less elegant, but far more realistic.

China’s export controls have exposed the uncomfortable truth that the modern economy depends on materials most people cannot name, processed through supply chains most investors have never seen, controlled by policies that can change with a government announcement.

The world is now trying to adapt.

Factories are rethinking inventories. Governments are building alliances. Industrial buyers are searching for alternative sources. Investors are beginning to understand that the critical minerals story is not a passing headline.

It is a structural shift.

And once again, the central point is simple:

The technologies of the future are only as secure as the materials behind them.

At Strategic Metals Invest, we help private investors understand and access selected rare earths and technology metals through physical ownership, professional storage, and established industrial supply chains.

Because in the new minerals race, owning the material itself may be one of the clearest ways to understand what is really at stake.

{kind=link}

{kind=link}

{kind=link}